Welcome to Financial Genius! Today I want to talk about a very simple but very important topic - supply and demand in the market. It is these two indicators that have a tremendous impact on many other economic values that are important for each individual person: prices, wages, inflation, devaluation, jobs, return on assets and much more. What are supply and demand, how are they related to each other, how are they characterized - you will learn about all this from today’s article.

So let's start with definitions. They will be very simple.

Demand– this is the desire and ability of the buyer to purchase a certain product or service from the seller.

Offer– this is the desire and ability of the seller to sell a certain product or service to the buyer.

Let me immediately draw your attention: the definitions contain two concepts: “desire” and “opportunity”, which must be considered together. If there is only desire and no opportunity, or vice versa, this cannot in any way influence supply and demand.

What determines supply and demand in the market?

Now let's look at what supply and demand in the market depend on, what factors influence them. We will consider them separately in the context of each category.

Factors influencing demand:

- People's income level. The higher it is, the higher the demand for goods and services. Moreover, the level of income most affects the demand for non-essential goods and services, goods and services of a high price category. But income levels have the least impact on everyday goods and services.

- Target market audience. The wider the target market audience for any product or service, the higher the demand for it, and vice versa. For example, the demand for bread will be orders of magnitude higher than the demand for aquarium fish.

- Season and fashion. Another important factor that has a tremendous impact on the demand for seasonal goods and services. For example, in summer the demand for sleds will be practically zero, but with the first snow it will increase significantly. As for fashion, this factor also always influences demand - this is one of the characteristic features of the world in which we all live now.

- Availability of analogues of goods and services, level of market monopolization. If a product or service is unique in its kind, the demand for it will always be higher than for goods and services that have many analogues. Also, the demand for the products of monopoly enterprises will also always be high. For example, on .

- Expectations of inflation and devaluation. And the last factor influencing demand, which is now becoming increasingly stronger, is expectations. When a person feels that the price of a product he needs will soon rise (inflation will occur), or his money will depreciate (devaluation will occur), he will try to buy it faster, to stock up even under current conditions. Thus, inflation expectations always stimulate an increase in demand for almost all goods, and actual inflation and devaluation, on the contrary, reduce demand, because the ability to make purchases (purchasing power) decreases.

Factors influencing supply:

- Production capabilities. The more goods or services resources, capacities, and technologies allow to be released onto the market, the greater the supply can be. However, the offer will not necessarily be the maximum, since it also depends on further factors.

- Tax policy. The softer the tax system for producers of goods and services, the more they will be produced, and the higher their supply on the market will be.

- Offer of related, complementary, and replacement products. If goods or services act as some kind of connecting link in a more complex production chain, or somehow complement other goods and services, then the supply of the main and additional goods will always be comparable. For example, the supply of bottles for lemonade will be focused on the volume of production of lemonade itself. Also, the more substitute goods there are on the market, the less supply of a particular product will be.

- Target market audience. This factor simultaneously affects supply and demand in the market. It makes no sense to offer a product or service more than it is in demand, so the narrower the target audience, the smaller the supply, and vice versa.

- Availability for business. The final supply factor I want to look at is the real opportunity to create goods and services. This includes the level and ease of opening and running a business, and everything connected with it. The easier it is to open and run a business, the higher the supply of goods and services will be.

Now that you have an idea of what supply and demand in the market depend on, let’s move on.

Law of supply and demand.

In economic theory there is such a thing as the law of supply and demand (sometimes it is divided into separate components: the law of demand and the law of supply). It is as follows.

Law of supply and demand: as the cost of goods and services increases, the demand for them falls, and supply increases, with other factors remaining constant.

Of course, this law is not ideal and cannot be strictly followed in all conditions. Since a decrease in demand and an increase in supply with rising prices will contradict each other, and at some point the reverse process may begin.

Therefore there is such a thing as supply and demand balance– this is a market situation in which these 2 parameters are optimally combined with each other.

Finding the equilibrium point between supply and demand is to increase the price of a product and the quantity of goods produced as much as possible, but until this leads to a drop in demand. This can be clearly depicted in the following graph:

Here you see supply and demand curves(as a rule, they are in just such an inverse, nonlinear relationship). Supply and demand curves show the dependence of these parameters on the quantity of a good or service and price.

The graph clearly shows how the law of supply and demand is observed: as the price of a product increases, supply increases and demand decreases. However, it is immediately clear that if the price increases excessively, the supply of the product will absolutely not correspond to the demand for it, and the higher the price increases, the stronger this discrepancy will be.

Therefore, the manufacturer of a product or service seeks the balance of supply and demand in the market, that is, the point on the graph where the supply and demand curves intersect. It is at this point that the manufacturer will earn the most, and the consumer will be satisfied with the price.

However, this is all good in theory. In practice, it often happens that a manufacturer or seller simply cannot keep the price at the level of equilibrium between supply and demand on the market, since, due to the action of other factors influencing supply, such a price will be unprofitable for him, since it will not even cover the cost.

Does demand determine supply or does supply determine demand?

And in conclusion, I would like to give my answer to this tricky question. What depends more on what: supply on demand or demand on supply?

In economic theory, the first answer has always been assumed: demand determines supply, the greater the demand, the greater the supply. In general, everything here is correct and logical.

However, in modern conditions, in the consumer society, which I already mentioned above, the opposite is often the case. That is, first a certain supply appears on the market, for which there is absolutely no demand yet, which may even be unknown to consumers, and this supply already generates demand. Roughly speaking, demand can be imposed on consumers in this way.

A typical example of this situation would be a selfie monopod. Just a few years ago, no one even knew what it was; the demand for this product was zero. And look how popular this thing is now!

Now you know what supply and demand are in the market, how they are formed, what factors influence them, and how they depend on each other. I hope that this information was useful to you and will contribute to the development of your financial literacy.

Stay tuned - here you will find a huge amount of other informative and interesting materials in the field of finance and economics. See you again!

What does the supply of goods depend on Dudaeva L.V. Homework: § 10 Theory Questions

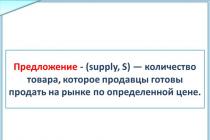

Dudaeva L.V. Supply - (supply, S) the quantity of goods that sellers are willing to sell on the market at a certain price.

Offer: price change P Q A C S B Increase Decrease S1S1 S2S Dudaeva L.V.

The amount of supply is directly dependent on the price: higher price higher supply lower price lower supply Law of supply Dudaeva L.V.

Changes in production technology Changes in prices for resources Prices for other goods Change in the number of sellers Inflationary expectations Introduction of additional taxes Changes in natural and climatic conditions Factors affecting supply Dudaeva L.V.

Dudaeva L.V. Elasticity of supply - shows by how many percent the volume of supply changes in response to a price change of one percent

Dudaeva L.V. Assignments 1. What will happen to the wheat supply curve when prices for mineral fertilizers increase 2. Suppose that a new technology has been introduced in steel production that provides cost savings. What will happen to the supply on the steel market? 3. How will sellers of foreign cars react to the introduction of import duties on goods?

Dudaeva L.V. Tasks 4. It is known that on the eve of the New Year, the rush demand for champagne leads to an increase in its price. How can champagne producers behave in October-November? 5. In recent years, many cafes and restaurants have appeared in Moscow. What can be said about the supply curve in the Moscow catering services market? 6. On the fertile lands of Ukraine, both wheat and buckwheat grow equally. Let's assume that the price of buckwheat has increased due to the fact that people have learned about its healing properties. How might this affect wheat supply?

Sections: Economy

Lesson objectives:

1. Educational :

Study the concepts of “supply”, “quantity of supply”, “law of supply”, supply scale, supply curve, non-price factors of supply, elasticity of supply, price elasticity coefficient of supply.

2. Developmental:

Development of attention, memory, reaction speed, ability to analyze simple and complex economic situations, expansion of economic horizons.

3. Educational:

Raising an economically literate citizen of his country.

Know:

- What is supply, quantity of supply.

- Understand the law of supply.

- What is price elasticity of supply?

Be able to:

- Explain the economic meaning of elasticity of supply.

- Depict graphically the supply curve and supply quantity (distinguish between movement along the curve and movement of the supply curve itself).

- Explain changes occurring in the market as a result of an increase or decrease in supply.

Lesson type: learning new material using information technology.

Lesson time: 2 hours (paired lesson).

Interdisciplinary connections: algebra, geometry, marketing.

Terms and concepts:

- Offer.

- Size of offer.

- Law of supply.

- Determinants of supply.

- Elasticity of supply.

- Supply curve.

Equipment:

- Computer, screen, projector.

- Disc with presentation (Appendix 1).

During the classes:

I. Organizational part of the lesson:

- Checking the presence of students, class attendants.

- Voice the topic of the lesson, goals.

II. Learning new material. Formation of new knowledge.

- The concept of a proposal.

- Offer scale. Constructing a supply curve.

- Formulation of the law of supply.

- Elasticity of supply. Factors of supply elasticity: price, non-price.

- Problem solving.

III. Consolidation of new material. Checking the mastery of basic concepts by completing a test task.

IV. Homework.

V. Literature for the lesson.

Lesson outline:

1. The concept of a proposal.

You can understand the laws of how the market works only by understanding what buyers are guided by in the market and what sellers are striving for.

In the market, people buy goods due to the fact that these goods are offered for sale by manufacturers.

Definition:

The quantity of goods that sellers offer for sale on the market during a certain period of time and at a certain level of market price is called the size of the offer.

What determines the quantity of supply? (question to students) On the prevailing price level in trade.

Offer- is the number of goods offered by the manufacturer for sale on the market (slide number 2).

Question for students: Which statement represents the concept of “sentence”, and which one represents the “magnitude of the supply”?

A. The quantity of a good that a firm is able and willing to sell at a given price at a given place and at a given time (Suggested answer: quantity supplied)

B. The intention and ability of sellers to bring goods to market for sale (Suggested answer: supply).

The teacher should draw students' attention to the fact that there are significant differences between the theories of supply and demand. The first is related to consumer preference and utility, the second is related to production. Therefore, one should not assume that the theory of supply is the theory of demand “on the contrary”.

2.

Supply scale

The effect of price on supply can be shown in the table (slide number 3).

3. Supply curve

The effect of price on supply can also be shown on a graph (slide number 4).

4. Law of supply (slide No. 5).

Based on the above material, the teacher invites students to independently formulate the law of supply.

5. Determinants of supply (slide No. 6, slide No. 7).

In addition to prices, there are other factors that influence the quantity of goods that sellers want to sell.

Factors that cause a change in supply and a shift in the supply curve - determinants of supply.

Using examples, it is necessary to analyze non-price factors of supply.

Examples could be the following:

1. Production costs change

Reducing prices for resources or improving the quality of used resources leads to a decrease in the cost of producing a unit of output and increases the supply of goods. The supply curve shifts to the right.

2. New equipment and technology are used.

The introduction of new methods of production of goods and services in production leads to an increase in supply. The supply curve shifts to the right.

3. A change in the price of the goods produced is expected.

If producers expect prices for their product to rise in the future, they may delay bringing products to market at today's lower prices, reducing supply. Graphically, this can be shown by a shift of the supply curve to the left.

You can then suggest discussing the remaining factors using student examples.

4. The number of sellers is increasing

5. Taxes are introduced or abolished

6. Prices for goods produced under similar conditions change

6. Test yourself – 1. Test (slide No. 8).

The test tests the assimilation of new concepts in the first part of the lesson: supply, quantity of supply, scale of supply, supply curve, law of supply, determinants of supply. Lagging students are identified. They may be given additional homework to better understand the material.

7. Price elasticity of supply (slide No. 10).

Discuss with students the concept of price elasticity of supply.

8. Formula for price elasticity of supply (slide No. 11).

Price elasticity of supply is a positive value, because As the price increases, the quantity supplied increases, which follows from the law of supply.

9. Types of price elasticity of supply. Time factor and elasticity

The supply function depends on the time period in question. (slide number 12).

Example: fishermen brought freshly caught fish to the market. Regardless of the price, they will not be able to increase the supply of fish on the same day, because they will not have time to go to sea again. Therefore, if the analyzed period is 1 day, then the supply curve will be vertical (slide number 16).

10. Elastic offer (slide No. 13).

11. Inelastic supply (slide No. 14).

12. Absolutely elastic offer (slide No. 15).

13. Absolutely inelastic supply (slide No. 16).

14. Problem solving (slide No. 17, slide No. 18).

15. Test yourself-2. Test (slide No. 19).

We summarize the lesson, consolidate the acquired knowledge by solving a test task.

We draw a conclusion from the lesson: guys, you have become familiar with the concepts of “demand” and “supply”. In your opinion, is there a relationship between them? What is it expressed in? (listening to students' answers). To summarize: in markets, supply and demand are formed under the influence of the interests of all buyers and sellers. It is necessary to remove obstacles to their free formation.

16. Homework (slide number 20).

Literature for the lesson.

- Azimov L.B. Teaching the course “Introduction to Economics”: a teacher’s manual. – M: “Vita-Press”, 1998.

- Fundamentals of economic theory: Textbook for grades 10-11 in general education institutions. Profile level of education / ed. S.I. Ivanova. – 8th ed., revised. - in 2 books. Book 1. – M.: Vita-Press, 2005.

- Teaching the course “Fundamentals of Economic Theory”: A manual for teachers of grades 10-11. educational institutions with in-depth study of economics / State. Univ. High School of Economics; edited by S.I. Ivanova. 2nd ed., Spanish - M.: Vita-Press, 2001.

- Workshop on the fundamentals of economic theory: Teaching. allowance for 10 – 11 grades. educational institutions with in-depth study of economics / State. Univ. High School of Economics; edited by S.I. Ivanova. 6th ed., - M.: Vita-Press, 2005.

- Savitskaya E.V. Economics lessons at school: in 2 books. Book 1. Manual for teachers. – M.: Vita-Press, 1998.

- Travin E.N. Economics lessons at school. A manual for teachers of economics and social studies - Yaroslavl: Development Academy, Academy Holding, 2003.

The goods they need due to the fact that these goods are offered for sale. But what determines the volume of goods offered for sale?

Supply quantity- the volume of a product of a certain type (in physical measurement) that sellers are ready (willing and able) to offer to the market during a certain period at a certain level of the market price for this product.

Studying the actions of sellers on the market, it is easy to notice that the quantity of goods that they offer for sale (the amount of supply) also directly depends on the price level that develops in trade.

Typically, the higher the price at which an economic good (a good in demand) can be sold, the more volume sellers and manufacturers are willing to offer to the market. This is quite logical: the more money the seller earns for the goods he sold, the more he can spend on satisfying his own desires, the more comfortable life he can achieve.

The relationship between the supply of goods and the price level at which these goods can be sold is illustrated in Fig. 3-3.

Rice. 3-3. Relationship between the supply of goods and the price level

As we can see, the higher the price, the more goods sellers are willing to offer to the market in exchange for buyers’ money. In other words, each price level on the market will correspond to its own supply of goods from sellers (producers).

The quantity supplied usually moves in the same direction as prices. And the entire set of possible supply values at different price levels forms the supply of certain goods on the market.

As with demand, the relationship between quantity supplied and supply is easier to understand if each is an answer to a specific question. The answer to the store owner’s question: “How many goods will manufacturers be willing to offer me for sale per month at a price equal to Xp?” - there will be information about the AMOUNT OF OFFER. If he poses the question differently: “How many goods will manufacturers be willing to offer me in a month at different price levels for this product?”, then the answer will be the characteristics of SUPPLY in this market.

Since the quantity supplied changes depending on the change in price, we can talk about price elasticity of supply.

Offer- the dependence that has developed in a certain period of the supply of a certain product on the market during a certain period (month, year) on the price level at which this product can be sold.

Price elasticity of supply- the scale of change in the quantity of supply (in %) when the price changes by one percent.

The degree of such elasticity is determined by dividing the difference (in %) in the quantities supplied before and after the price change by the amount of the price change (in %). Levels of elasticity of supply also differ among goods, and therefore price changes of the same relative magnitude can cause unequal increases in the supply of different goods.

Table 3-2

Information about possible supply quantities is usually presented graphically in the form of a curve called the supply curve. It describes the picture of supply in a given product market, that is, the relationship between:

- price of the goods and

- volumes of its production (supplies to trade) possible at different price levels.

Let's construct a supply curve (Fig. 3-4) based on the data in Table 3-2 (this kind of table is usually called supply scales).

Rice. 3-4. Supply curve (using the example of the bicycle market)

Each point on this curve is the amount of supply of a given product (possible production volume) at a certain level of its price. For example, a point with coordinates (70, 1300) means that at a price of 1300 den. units manufacturers are ready to offer 70 bicycles for sale

Thus, the supply curve (see Figure 3-4) allows you to answer two questions:

- What will be the quantity supplied at different price levels?

- How will the quantity supplied change if the price changes slightly?

Therefore, any manufacturer (seller), when getting down to business, must begin by looking for answers to the following questions:

- Will the sales revenue justify the costs associated with the production (organization of sales) of this product?

- Will the production (sale) of this product bring him personal income and, if so, what kind?

As a rule, an increase in prices causes an increase in the number of goods offered for sale, and a decrease in prices causes a decrease in this number.

Economists call this pattern of behavior of producers (sellers) in the markets of most goods the law of supply.

Law of supply: An increase in prices usually leads to an increase in the quantity supplied, and a decrease in prices usually leads to a decrease.

Along with price, the supply of goods is also influenced by factors such as:

- prices of other goods (and therefore the profitability of their production);

- prices of factors of production used to produce a given product;

- technology, i.e. methods of manufacturing a product or organizing the provision of a service.

It is easy to see that the logic of behavior in the market of both buyers and producers of goods is opposite: when prices rise, producers and sellers are ready to offer an increasing amount of goods to the market, while buyers respond to rising prices by reducing the quantity of demand.

This contrast in the reaction of supply and demand is generated by opposing interests that bring buyers and sellers to the market.

Buyers want to purchase as many goods as possible with the limited amount of money they have. Sellers, on the contrary, want to get as much money as possible for their limited volume of goods.

How the market reconciles these conflicting interests of buyers and sellers will be discussed in the next chapter.

But first, let's formulate another recipe for economic prudence.

Recipe three

It is necessary to remove obstacles to the free formation of supply and demand in markets under the influence of the interests of all buyers and sellers.

Slide 1

What is incorrect in the following statement? Cold weather has reduced the demand for hotel rooms on the Black Sea coast, thereby reducing the price of renting a room. The fall in rental price, in turn, caused an increase in demand, so that eventually the price returned to its original levelSlide 2

Answer: In this statement, the concepts of “demand” and “quantity of demand” are confused. It would be more correct to say that cold weather led to a decrease in demand for rooms, since in this case demand will change at any price level. A fall in price, on the contrary, will cause an increase in the quantity demanded.

Answer: In this statement, the concepts of “demand” and “quantity of demand” are confused. It would be more correct to say that cold weather led to a decrease in demand for rooms, since in this case demand will change at any price level. A fall in price, on the contrary, will cause an increase in the quantity demanded.

Slide 3

Katya loves butter and thinks margarine tastes like soap. Grigory does not feel the difference between them. Whose demand for butter should be more price elastic? Justify your answer.

Katya loves butter and thinks margarine tastes like soap. Grigory does not feel the difference between them. Whose demand for butter should be more price elastic? Justify your answer.

Slide 4

Answer: For Katya, margarine is not a substitute for butter in consumption, but for Gregory it is a substitute product. Consequently, Gregory's demand for butter will be more elastic than Katya's demand. If the price of butter increases, Grigory will stop consuming it and switch to margarine. Katya will begin to buy butter at higher prices, only slightly reducing its consumption

Answer: For Katya, margarine is not a substitute for butter in consumption, but for Gregory it is a substitute product. Consequently, Gregory's demand for butter will be more elastic than Katya's demand. If the price of butter increases, Grigory will stop consuming it and switch to margarine. Katya will begin to buy butter at higher prices, only slightly reducing its consumption

Slide 5

Slide 6

Supply is the desire and ability to produce and sell a given product (service) at a given price at a given time.

Supply is the desire and ability to produce and sell a given product (service) at a given price at a given time.

Slide 7

LAW OF SUPPLY THE AMOUNT OF SUPPLY IS DIRECTLY DEPENDENT ON THE CHANGE IN THE PRICE OF A GOODS (supply increases with an increase in price and falls when it decreases)

LAW OF SUPPLY THE AMOUNT OF SUPPLY IS DIRECTLY DEPENDENT ON THE CHANGE IN THE PRICE OF A GOODS (supply increases with an increase in price and falls when it decreases)

Slide 8

Slide 9

WHAT AFFECTS THE AMOUNT OF SUPPLY? 1. Manufacturer’s costs 2. Technology used 3. Expectation of an increase in the price of the product

WHAT AFFECTS THE AMOUNT OF SUPPLY? 1. Manufacturer’s costs 2. Technology used 3. Expectation of an increase in the price of the product

Slide 10

When supply increases, the curve shifts down and to the right (S1); when supply falls, it shifts up and to the left (S2).

When supply increases, the curve shifts down and to the right (S1); when supply falls, it shifts up and to the left (S2).

Slide 11

Elasticity of supply - the scale of change in the quantity of supply (in %) when the price changes by one percent

Elasticity of supply - the scale of change in the quantity of supply (in %) when the price changes by one percent

Slide 12

What will happen to the wheat supply curve if mineral fertilizer prices increase? Higher prices for mineral fertilizers will increase wheat production costs. This means that while maintaining the same market price for wheat, farmers will be able to offer less of their product for sale. A decrease in the supply of wheat as a result of rising prices for mineral fertilizers should be demonstrated by a shift in the supply curve to the left

What will happen to the wheat supply curve if mineral fertilizer prices increase? Higher prices for mineral fertilizers will increase wheat production costs. This means that while maintaining the same market price for wheat, farmers will be able to offer less of their product for sale. A decrease in the supply of wheat as a result of rising prices for mineral fertilizers should be demonstrated by a shift in the supply curve to the left

Slide 13

Suppose that a new technology is introduced in steel production that provides cost savings. What will happen to the supply on the steel market? The introduction of new, progressive technology will reduce the cost of producing each additional ton of steel. At the prevailing market price, producing these additional tons of steel will become more profitable and the supply of steel will increase, which will be reflected by a shift of the market supply curve to the right

Suppose that a new technology is introduced in steel production that provides cost savings. What will happen to the supply on the steel market? The introduction of new, progressive technology will reduce the cost of producing each additional ton of steel. At the prevailing market price, producing these additional tons of steel will become more profitable and the supply of steel will increase, which will be reflected by a shift of the market supply curve to the right

Slide 14

It is known that on the eve of the New Year, the rush for champagne usually leads to an increase in its price. How can champagne producers behave in October-November? Manufacturers' expectation of price increases on the eve of the New Year may lead to a reduction in the supply of sparkling wines in October-November. Manufacturers will prefer to keep some of their products in stock in order to sell them at higher prices in December.

It is known that on the eve of the New Year, the rush for champagne usually leads to an increase in its price. How can champagne producers behave in October-November? Manufacturers' expectation of price increases on the eve of the New Year may lead to a reduction in the supply of sparkling wines in October-November. Manufacturers will prefer to keep some of their products in stock in order to sell them at higher prices in December.

Slide 15

Wheat and buckwheat grow equally well on the fertile lands of Ukraine. Suppose that the price of buckwheat has increased sharply due to the fact that people have learned about its healing properties. How might this affect wheat supply? Changing the prices of other goods that can be produced using the same resources can also shift the supply curve. An increase in prices for buckwheat will lead to producers devoting a larger area to buckwheat crops and a smaller area to sow wheat. Consequently, the supply of wheat will decrease and the supply curve will shift to the left. Task. Population demand function for this product: Qd=7-P. Supply function: QS = -5 + 2 P, where Qd is the volume of demand in millions of pieces per year; Qs - supply volume in millions of pieces per year; P - price in thousands of rubles. Construct graphs of supply and demand for a given product, plotting the quantity of the product (Q) on the abscissa axis and the unit price of the product (P) on the ordinate axis.

Wheat and buckwheat grow equally well on the fertile lands of Ukraine. Suppose that the price of buckwheat has increased sharply due to the fact that people have learned about its healing properties. How might this affect wheat supply? Changing the prices of other goods that can be produced using the same resources can also shift the supply curve. An increase in prices for buckwheat will lead to producers devoting a larger area to buckwheat crops and a smaller area to sow wheat. Consequently, the supply of wheat will decrease and the supply curve will shift to the left. Task. Population demand function for this product: Qd=7-P. Supply function: QS = -5 + 2 P, where Qd is the volume of demand in millions of pieces per year; Qs - supply volume in millions of pieces per year; P - price in thousands of rubles. Construct graphs of supply and demand for a given product, plotting the quantity of the product (Q) on the abscissa axis and the unit price of the product (P) on the ordinate axis.