4-FSS for the 4th quarter of 2018 - it is worth downloading the completed sample in order not to make mistakes when filling out a fresh report to the FSS. You can do this in our article. From it you will also learn how the 4-FSS form has changed for the current reporting campaign, and you will also see all the nuances of its design.

The evolution of the 4-FSS form since 2017 and its latest (new) form

The report, compiled according to Form 4-FSS, reflects information on the accrual/payment of contributions for injury insurance and, since 2017, is the only report on contributions submitted to this extra-budgetary fund. This is due to the fact that control over the payment of the main volume of insurance premiums (accrued on payments intended for the Social Insurance Fund in relation to disability and maternity insurance, Pension Fund of the Russian Federation, Compulsory Medical Insurance) has been transferred to the tax authorities since the beginning of 2017. However, “unfortunate” contributions in all aspects remained under the jurisdiction of the FSS.

Since the report on contributions submitted to social security before these changes also contained data on payments transferred under the control of the tax service, its form had to be shortened, removing from it the sections reserved for information that was no longer transferred to the fund by the payer of contributions. But the report retained its short name and is still called Form 4-FSS.

The form of this report used in 2018 and the procedure for entering data into it, which underwent a similar adjustment, were approved by order of the Federal Social Insurance Fund of the Russian Federation dated September 26, 2016 No. 381. In the original edition, the abbreviated form of Form 4-FSS was used when preparing 2 reports: for 1 quarter and for half a year 2017.

Since July 2017 (order of the FSS of the Russian Federation dated 06/07/2017 No. 275), the updates made in the text of order No. 381 have come into force, the application of which turned out to be possible only from the report for 9 months of 2017 (information of the FSS of the Russian Federation “On the application of the order of the FSS of the Russian Federation dated 06/07/2017 No. 275"). Since then the form has not changed. That is, Form 4-FSS for the 4th quarter of 2018 is a form entered from the report for the 3rd quarter of 2017.

With the latest update, a little has changed in it and not for each of the payers:

- codes for sources of funds that must be indicated by the budget organization have been added to the title page;

- additional lines have been introduced into the table reflecting the turnover of settlements related to contributions to reflect the debt of the employer or fund to it resulting from the reorganization of a legal entity or the closure of its separate division.

Corresponding amendments have been made to the text of the procedure for filling out the form.

Read about what the current form looks like and where the information to be entered into its tables comes from in this article.

Features that arise when registering 4-FSS

Filling out form 4-FSS does not have any significant differences in the rules of execution from other reporting forms. It is the same as in other reports:

- there are mandatory and optional tables to fill out and submit;

- absence of data to be filled in is marked with a dash;

- It is possible to make adjustments if errors are identified.

This report acquires a number of features when it is filled out by policyholders - participants in a pilot project that provides for insurance payments from the fund not to the policyholder, but directly to the insured individual. These features are connected with the fact that these persons do not need to fill out information about payments made by social insurance. This process has a certain influence on the moment the insurer enters the pilot project. The details of entering data on payments from the fund into the report are covered in the order of the Federal Social Insurance Fund of the Russian Federation dated March 28, 2017 No. 114.

Sample of filling out 4-FSS for the 4th quarter of 2018

It is generally incorrect to call a report to the Social Insurance Fund, submitted to the fund quarterly, a quarterly report. It is compiled on an accrual basis for the year (taking into account all accruals, transfers, payments made during the year), and its reporting periods correspond in length to the number of months that have passed since the beginning of the year.

However, the information added in relation to the last quarter of the reporting period is newly introduced into the next report, and it is this information that is detailed in numbers in tables 1, 1.1 and 2 of the form. Therefore, the name of the reporting period corresponding to the next quarter appears in everyday life.

A sample of the 4-FSS report for the 4th quarter. 2018 (or rather, for the entire 2018) is available for viewing and downloading on our website:

Results

The report on Form 4-FSS, used in 2018, is already familiar to policyholders, since it has been used without changes since the 3rd quarter of 2017. There are some specific features of filling it out for policyholders who are participants in the pilot project, which provides for the “direct” receipt of insurance payments from the fund by the insured individual.

Has the new 4-FSS form been approved for 9 months of 2017? What's new in the form? In this material you can learn about changes in the calculation of 4-FSS and download the new 4-FSS form (in the latest edition) for free.

What is 4-FSS in 2017

All organizations and entrepreneurs that pay citizens remuneration subject to compulsory social insurance contributions (Clause 1, Article 24 of Law No. 125-FZ of July 24, 1998) must submit calculations using Form 4-FSS.

Form 4-FSS is a Calculation of accrued and paid insurance premiums for compulsory social insurance against accidents at work and occupational diseases, as well as expenses for the payment of insurance coverage. Since 2017, a new form 4-FSS has been in force, approved by FSS Order No. 381 dated September 26, 2016.

The 4-FSS report form includes:

- title page;

- table 1 “Calculation of the base for calculating insurance premiums”;

- Table 1.1 “Information required for calculating insurance premiums by policyholders specified in paragraph 21 of Article 22 of the Federal Law of July 24, 1998 No. 125-FZ.” (for situations where employees are temporarily employed in another organization or with an individual entrepreneur);

- table 2 “Calculations for compulsory social insurance against accidents at work and occupational diseases”;

- Table 3 “Expenses for compulsory social insurance against accidents at work and occupational diseases”;

- table 4 “Number of victims (insured) in connection with insured events in the reporting period”;

- Table 5 “Information on the results of a special assessment of working conditions and mandatory preliminary and periodic medical examinations of workers at the beginning of the year.”

New reporting form for 9 months

From 06/07/2017, by FSS Order No. 275, some changes were made to the calculation form, which will need to be taken into account when preparing Form 4-FSS for 9 months of 2017. Let's tell you more about them.

New field “Budget organization”

The “Budget Organization” field appeared on the title page, where such organizations must indicate the source of funding. There was no such field before. Now you need to indicate from which source the funding comes. The corresponding codes are provided for this:

- Federal budget;

- Budget of a constituent entity of the Russian Federation;

- Municipal budget

- Mixed financing.

New line about the policyholder's debt

Line 1.1 “Debt owed by a reorganized policyholder and (or) deregistered separate division of a legal entity” has been added to Table 2.

On a new line in accordance with Article 23 of the Federal Law of July 24, 1998 No. 125-FZ, the policyholder - legal successor reflects the amount of debt transferred to him from the reorganized insurer in connection with the succession, and (or) the legal entity reflects the amount of debt deregistered separate division.

New line about debt owed to the Social Insurance Fund

Table 2 also includes line 14.1 “Debt of the territorial body of the Fund to the policyholder and (or) a separate division of the legal entity deregistered.” According to it, the legal successor reflects the amount of debt owed to the territorial body of the Social Insurance Fund, which was transferred to it from the reorganized insurer in connection with the succession, as well as the amount of debt owed to the territorial body of the Social Insurance Fund of the separate division deregistered.

You can free of charge a new form of calculation of 4-FSS, used for reporting for 9 months of 2017, in Excel format.

Filling rules: what has changed

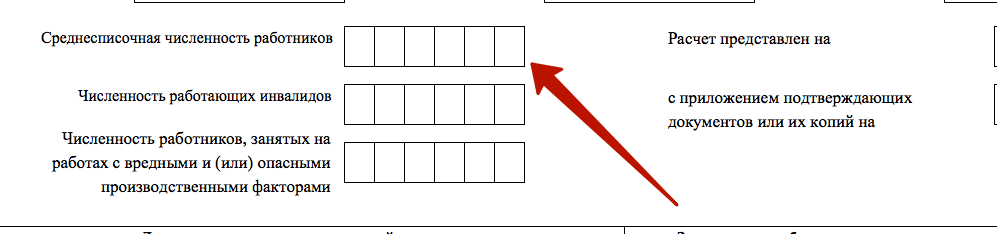

On the title page there is a field to reflect the “Average number of employees”:

The adopted amendments clarify that in the “Average number of employees” field on the title page of the Calculation, the indicator is calculated for the period from the beginning of the year. Previously, filling out this field raised questions: it was not entirely clear whether it needed to be filled out from the beginning of the year or only for the last three months of the reporting period.

You can use an example of filling out the 4-FSS calculation for the 3rd quarter of 2017.

All organizations, as well as those individuals (including individual entrepreneurs) who have entered into employment contracts with employees or GPC agreements providing for the payment of contributions for injuries, are required to submit a Calculation in Form 4-FSS (Article 3, paragraph 1 Article 24 of the Federal Law of July 24, 1998 No. 125-FZ). We will tell you about the timing, form of presentation of the Calculation, the procedure for filling it out in our consultation, and also give an example of a completed form 4-FSS for 9 months of 2017.

Form 4-FSS for 9 months 2017

Form 4-FSS is a Calculation of accrued and paid insurance premiums for compulsory social insurance against accidents at work and occupational diseases, as well as expenses for the payment of insurance coverage. Let us remind you that from January 1, 2017, a new form 4-FSS, approved by FSS Order No. 381 dated September 26, 2016, has been in effect. For the first time, policyholders submitted it for the 1st quarter of 2017.

It must be borne in mind that on 06/07/2017, by FSS Order No. 275, some changes were made to the Calculation form, which will need to be taken into account when preparing Form 4-FSS for 9 months of 2017.

The new form, submitted for 9 months of 2017, compared with the Calculation for the 1st quarter and half of 2017, includes, in particular, the following changes (FSS Order No. 275 dated 06/07/2017):

- the “Budget Organization” field appeared on the title page, where such organizations must indicate the source of funding;

- line 1.1 “Debt owed by a reorganized policyholder and (or) deregistered separate division of a legal entity” has been added to Table 2;

- Table 2 also includes line 14.1 “Debt of the territorial body of the Fund to the policyholder and (or) a separate division of the legal entity deregistered.” According to it, the legal successor reflects the amount of debt owed to the territorial body of the Social Insurance Fund, which was transferred to it from the reorganized insurer in connection with the succession, as well as the amount of debt owed to the territorial body of the Social Insurance Fund of the separate division deregistered.

It is also clarified that in the “Average number of employees” field on the title page of the Calculation, the indicator is calculated for the period from the beginning of the year.

Please note that the Calculation is presented for the reporting period, which recognizes the first quarter, half-year, nine months of the calendar year, calendar year (Clause 2 of Article 22.1 of the Federal Law of July 24, 1998 No. 125-FZ). This means that form 4-FSS is compiled on an accrual basis. Therefore, talking, for example, about the 4-FSS form for the 3rd quarter of 2017 is not entirely correct. More correctly, about the form for 9 months of 2017. However, for convenience, thereby denoting the last quarter, the data for which are presented in detail in the Calculation form, we will consider the Calculations for the 3rd quarter and 9 months as equivalent.

For the 4-FSS report for the 3rd quarter of 2017, the Excel form can be downloaded.

Let us remind you that if policyholders need to submit an updated Calculation for periods before 2017, then it is necessary to use the form of the forms that were in force in the relevant periods (clause 1.5 of Article 24 of the Federal Law of July 24, 1998 No. 125-FZ).

New form 4-FSS for 9 months of 2017: how to submit and when

The calculation in form 4-FSS is submitted by policyholders to the territorial body of the FSS at the place of their registration. In this case, the following deadlines are established (clause 1, article 24 of the Federal Law of July 24, 1998 No. 125-FZ):

- on paper - no later than the 20th day of the month following the expired quarter;

- in electronic form - no later than the 25th day of the month following the expired quarter.

The following can submit Calculations on paper:

- insurers whose average number of individuals in whose favor payments and other remunerations are made did not exceed 25 people for the previous year;

- newly created (including during reorganization) organizations in which the number of the above individuals does not exceed 25 people.

Thus, the 4-FSS calculation for 9 months of 2017 must be submitted no later than:

- 10/20/2017, if the Calculation is submitted on paper;

- 10/25/2017 when submitting the form electronically.

Composition of the 4-FSS form for the 3rd quarter of 2017

Form 4-FSS contains both mandatory sheets and tables that are always submitted, and tables that are filled out and submitted only if there is data to fill them out (let’s call them “additional”):

| Required sheet and tables | Additional tables |

|---|---|

| Title page | Table 1.1 “Information required for calculating insurance premiums by policyholders indicated...” |

| Table 1 “Calculation of the base for calculating insurance premiums” | Table 3 “Expenditures on compulsory social insurance against accidents at work and occupational diseases” |

| Table 2 “Calculations for compulsory social insurance against accidents at work and occupational diseases” | Table 4 “Number of victims (insured) in connection with insured events in the reporting period” |

| Table 5 “Information on the results of the special assessment of working conditions...” |

General requirements for filling out Calculation 4-FSS

Let's talk about some of the requirements for filling out form 4-FSS when submitting it on paper. The calculation can be filled out either on a computer and printed on a printer, or filled out by hand in block letters with a ballpoint or fountain pen in black or blue.

Only one indicator is entered in each line and its corresponding column. If there is no indicator, a dash is added.

If an error is made in the 4-FSS form, the incorrect value is crossed out and the correct value is entered. The correction is certified by the signature of the policyholder or his representative indicating the date of correction. If the policyholder has a seal, the corrections must be certified with it.

Correction of errors by correction or other similar means is not permitted.

After the form in the required volume of tables has been prepared, sequential numbering of the completed pages is entered in the “page” field in the Calculation. On each completed page, at the top, you must fill in the fields “Insured Registration Number” and “Subordination Code.” You can find this data in the notification (notice) received by the policyholder upon registration with the territorial body of the Social Insurance Fund.

At the bottom of each page of the Calculation is the signature of the policyholder (his representative) and the date of signing is indicated.

The procedure for filling out the Title Page and Calculation Tables 4-FSS can be found in Appendix No. 2 to FSS Order No. 381 dated September 26, 2016.

For policyholders who are registered with the Social Insurance Fund of the constituent entities of the Russian Federation participating in the pilot project, the specifics of filling out form 4-FSS are approved by the Social Insurance Fund Order No. 114 dated March 28, 2017.

Form 4-FSS for 9 months: sample filling

Let us present, using conventional digital data, a sample of filling out the 4-FSS for 9 months of 2017. Please note that when preparing 4-FSS for the 3rd quarter of 2017, you must indicate reporting period code 09 on the form.

We present Form 4-FSS for the 3rd quarter of 2017 (sample) as part of only the mandatory tables.

On June 7, 2017, Social Insurance issued a new Order No. 275, which updated the Calculation. The updated form 4-FSS should be used when submitting information for 9 months of 2017

Companies and merchants who are insurers for their employees, with whom employment contracts or GPC agreements have been concluded, providing for the payment of contributions “for injuries”, must report quarterly to Social Insurance in form 4-FSS. The form submitted for 9 months of 2017 has undergone a number of changes, we will tell you about them, and also remind you of the deadlines and procedure for submitting the Calculation to the Social Insurance Fund.

You can read about some of the nuances of filling out form 4-FSS on our forum:

What has changed in the 4-FSS form since the 3rd quarter of 2017?

Form 4-FSS has already changed this year; since January 1, 2017, the form approved by FSS Order No. 381 dated September 26, 2016 has been in effect. It was submitted for the 1st quarter of 2017.

On June 7, 2017, Social Insurance issued a new Order No. 275, which updated the Calculation. The updated Form 4-FSS should be used when submitting information for 9 months of 2017.

The following changes have been made:

- The title page is supplemented with the line “Budgetary organization”; state employees enter the source of their funding into it.

- In Table 2, a new line 1.1 has appeared “Debt due to a reorganized policyholder and (or) a separate division of a legal entity deregistered”;

- Line 14.1 has been added to Table 2: “Debt from the territorial body of the Fund to the policyholder and (or) a separate division of a legal entity that has been deregistered.”

In addition, the Rules for filling out Form 4-FSS specify that the line “Average number of employees” on the title page must be filled in with information about the number of employees for the period from the beginning of the calendar year.

In total, there are five tables and a title page in the 4-FSS form, of which the Title Page and Tables 1, 2, 5 are mandatory. Tables 1.1, 3 and 4 are filled out if the indicators required by their content are available.

Let us remind you that the reporting periods in Form 4-FSS are the first quarter, six months, 9 months and the calendar year. Thus, you need to fill out the form on a cumulative basis.

Don’t forget, if you need to submit an updated form to Social Security for periods before the current year, you should use the forms that were in force in the relevant periods.

How and when to submit Form 4-FSS?

The new 4-FSS calculation form must be submitted to the territorial Social Insurance office at the place of registration of the company or individual entrepreneur. The deadlines for submitting data have not changed; you need to report for 9 months:

- on paper - no later than October 20, 2017;

- in electronic format - until October 25, 2017.

Policyholders with an average number of employees of less than 25 people are allowed to report on paper. The rest are required to submit Calculations electronically using TKS.

Bukhsoft "Salaries and Personnel" is a convenient and functional program for filling out and checking 4-FSS. Try preparing calculations using Form 4-FSS online now!

Fine for late submission of reports to the Social Insurance Fund

Let us remind you that for violation of the deadlines for submitting reports to Social Security, penalties are provided. In particular, for delay in submitting Form 4-FSS, the policyholder faces a fine of 5% of the amount of injury contributions for each full or partial month of delay. The fine cannot be more than 30% of the amount of “traumatic” contributions and less than 1 thousand rubles.

If the policyholder is required to report electronically, but submitted information on paper, the fine will be 200 rubles.

It is worth noting that for violation of the deadlines for submitting information to government agencies, administrative liability is also provided, namely: from 300 to 500 rubles per official, according to Part 2 of Art. 15.33 Code of Administrative Offenses of the Russian Federation.

Form 4-FSS - a sample of filling out for the 1st quarter of 2019 with zero data you can see in our material. Here you will find a description of the mechanism for filling out such a report, find out which sheets do or do not need to be completed, and receive other important information on drawing up a zero 4-FSS.

What does the legislation say about zero 4-FSS?

Reporting to social security in Form 4-FSS is a calculation presented in tabular form, containing information:

- on insurance premiums for compulsory insurance against accidents at work and occupational diseases (ASP and OPD), accrued and paid in the reporting period (for injuries);

- expenses for payment of insurance coverage under NSP and PZ.

Zero calculation 4-FSS is a type of insurance reporting in the absence of reporting data. This situation arises if the company has suspended, ceased or is just planning to start operations.

The condition for the mandatory submission of such a calculation is contained in Art. 24 of the Law “On compulsory social insurance against accidents at work and occupational diseases” dated July 24, 1998 No. 125-FZ. This article speaks of the need for quarterly reporting on insurance premiums by all policyholders.

Find out who is taking the 4-FSS from this article.

Please note: an individual entrepreneur without employees does not submit a zero card to the Social Insurance Fund, since he is not an insurer.

There is no mention of zero form 4-FSS in the law. Nothing is said about this type of reporting in the FSS order No. 381 dated September 26, 2016, which describes the technology for filling out this reporting form.

However, this does not mean that the lack of reporting data relieves policyholders from submitting 4-FSS - everyone needs to report every reporting quarter. We will tell you how to do this in the following sections.

Mandatory zero sheets

Social insurance expects 4-FSS from policyholders in any case - whether they made payments in the reporting period in favor of individuals or not. If there is nothing to write down in the report, the employer will be required to submit a 4-FSS zero calculation completed according to special rules.

Its main difference from a regular (data-filled) calculation is the reduced volume of tables presented.

Calculation 4-FSS - 2019 is filled out on the form approved by. by order of the FSS dated September 26, 2016 No. 381, as amended. from 06/07/2017. You can download it below.

The minimum set of sheets and tables of the report is defined in clause 2 of Appendix No. 2 to Order No. 381 - it includes:

- title page;

- 3 tables (1 - calculation of the base for calculating insurance premiums, 2 - calculation of injury premiums and 5 - results of assessing working conditions).

These are mandatory sheets for 4-FSS. The remaining calculation tables (1.1, 3 and 4) may not be filled out - this is indicated in clause 2 of the Procedure for registration of 4-FSS, approved. by order No. 381 (Appendix No. 2). Therefore, you can create a zero calculation without them.

We will talk about the specifics of filling out the cells of the zero calculation tables in the next section.

How to prepare a report if there is no data - zeros, dashes or empty cells?

To correctly fill out the zero calculation in Form 4-FSS, use the algorithm set out in Appendix No. 2 to Order No. 381:

|

Clause of Appendix No. 2 to Order No. 381 |

Decoding |

|

Dashes are added to table cells if there is no reporting indicator. |

|

|

When filling out the “TIN” field in the 2 initial cells (zone of 12 cells), enter zeros (00) if the TIN consists of 10 characters. How to find out the FSS registration number by TIN in a couple of minutes, see the material |

|

|

In the 1st and 2nd cells of the field “OGRN (OGRNIP) of the legal entity, enter zeros (their OGRN consists of 13 characters with a 15-digit zone to be filled in) |

In addition, individual calculation cells are not filled in at all - neither with zeros nor dashes. For example:

- the field “Cessation of activity” located on the title page - according to clause 5.6 of Appendix No. 2 to Order No. 381, code “L” is entered in this field (if the company or individual entrepreneur is liquidated in the reporting period) or it is not filled in at all;

- field “Budgetary organization” - only state employees work with it (clause 5.12 of Appendix No. 2 to Order No. 381), and in the reporting of other companies and individual entrepreneurs it remains blank.

From these features of the calculation filling technique, the following conclusion can be drawn:

- zeros are entered only in the 1st and 2nd cells of the “TIN” and “OGRN” fields if the value indicated in them consists of 10 or 13 characters, respectively;

- In the cells of the form tables, if there is no data, dashes are inserted;

- individual cells for a specific purpose are left unfilled.

If you generate several different reports in parallel at once, read the next section to protect yourself from errors.

Technology of filling out calculations - how not to make a mistake?

The above method of filling out the fields is typical only for 4-FSS. When preparing, for example, the calculation of contributions, a different scheme is used (clause 2.20 of Appendix No. 2 to the Federal Tax Service order No. ММВ-7-11/551@ dated 10.10.2016):

- 12 acquaintances of the “TIN” field of a single calculation for insurance premiums must be filled out from the first cells, and with a 10-digit TIN, dashes are entered in the last 2 cells (for example, 8970652349--);

- missing indicators (quantitative and total) are filled with zeros; in other cases, empty cells are crossed out.

For a sample of a zero single calculation for insurance premiums, please see the link.

Do not confuse these technical features of the design of different reporting forms, otherwise problems may arise with the timely acceptance of the 4-FSS calculation by social insurance specialists. They may not accept the calculation on formal grounds - due to non-compliance with the procedure established by law for filling it out.

Find out how much the policyholder will have to pay if, due to a technical or other error, the calculation is not submitted on time.

When are numerical values entered in the zero report tables in the absence of “insurance” charges and payments?

The described scheme for filling out the calculation (namely, putting dashes in those table cells for which there are no indicators) cannot be used using the continuous method. That is, when filling out the zero calculation of 4-FSS, it is also necessary to take into account the peculiarities of filling out individual cells. Including:

|

Calculation cell 4-FSS |

Explanation for filling |

|

|

Row 5 of table 1 |

The line cannot be crossed out (there is information to fill it out) - write down the insurance rate in it, which is set for each policyholder depending on the class of professional risk. How the tariffs indicated in 4-FSS are set and what they depend on, find out |

|

|

Rows 6 and 7 of Table 1 |

Cross out the lines only if the tariff does not include a discount or surcharge |

|

|

Line 8 of table 1 |

If you have received a tariff premium, in line 8 indicate the date of the corresponding FSS order |

|

|

Line 9 of table 1 |

Always fill out the line - it will reflect:

|

|

|

Row 1 of table 2 |

In the line, enter the amount of debt to social insurance for contributions from NSP and PZ at the beginning of the billing period (if there is such a debt) - it is reflected in the accounting (for loan account 69) and confirmed by the results of reconciliation with the fund. Compare it with the amount reflected on page 19 of the 4-FSS calculation for the previous year - the indicators should match |

|

|

Row 3 of table 2 |

Fill out this line if the Social Insurance Fund has accrued injury contributions based on the results of desk or on-site inspections |

|

|

Row 4 of table 2 |

Expenses not accepted for offset by the Social Insurance Fund for previous billing periods based on inspection reports are reflected here. |

|

|

Row 5 of table 2 |

On this line, reflect the amount of contributions accrued by you for previous billing periods that are subject to payment (if any such accruals exist) |

|

|

Row 6 of table 2 |

Fill out this line if your account has received reimbursement from social insurance that exceeds the amount of accrued injury contributions. |

|

|

Row 7 of table 2 |

The line is filled in by companies and individual entrepreneurs if they have received a refund of overpaid contributions from social insurance. |

|

|

Row 8 of table 2 |

The line contains a numeric value, if pages 1-7 (or some of them) reflected non-zero values - the indicators on pages 1-7 are summed |

|

|

Lines 9,14.1 of table 2 |

These lines reflect the debts of the Social Insurance Fund to the policyholder (at the end and beginning of the billing period) |

Find out the technology for preparing the latest table 4-FSS in the next section.

Where can I get the information for Table 5?

Always fill out this table, regardless of whether the indicators are in the other calculation tables or not. It is devoted to the results of a special assessment of working conditions (SOUT) and mandatory medical examinations performed at the beginning of the year.

Please put dashes in all cells if you have registered as an insured this year. Other companies and individual entrepreneurs need to collect information:

- from the personnel service - about the number of jobs (this information is needed for column 3), the number of employees required to undergo medical examinations (column 7) and those who have already passed them (column 8);

- from the SAW report - on the number of certified workplaces, including those classified as harmful and dangerous working conditions (columns 4-6).

We'll tell you what the law on SOUTH refers to as harmful working conditions.

Sample 4-FSS with an example for a novice policyholder

Let's consider the scheme for filling out the 4-FSS 2019 for a company created in the 3rd quarter.

Example

Initial data:

- Stroika Plus LLC was registered in August 2019.

- At the end of the 3rd quarter, activities had not yet begun, staff had not been recruited, payments had not been made, insurance premiums had not been paid.

- Only the director is on staff.

- The injury contribution rate is 2.3% (without discounts or surcharges).

- The SOUT is scheduled for December 2019.

Despite the lack of activity, in October 2019 the company will be required to submit its first calculation to social insurance in Form 4-FSS. It will be null because there is no data to fill:

- table 1—no injury payments were accrued;

- table 2 - Stroika Plus LLC did not conduct mutual settlements with the Social Insurance Fund;

- table 5—there is no information about the results of special assessment tests and mandatory medical examinations.

How to complete a zero calculation, see the sample of filling out 4-FSS, latest edition 2019.

Results

All policyholders fill out the 4-FSS calculation form. If they did not work during the reporting period or temporarily suspended their work, they must submit a zero calculation on this form. If there is no reporting data, you need to fill out 3 mandatory tables (1, 2 and 5).